Telemus Weekly Market Review July 25th - July 29th, 2022

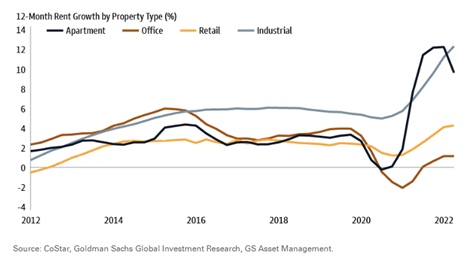

Location, location, location is the phase we’ve all heard when it comes to real estate investing and rightly so, just like earnings to a stock or credit worthiness to a bond, a structure’s location, is an important variable. But there is more to the story, particularly as the workforce has become more geographically nimble than was acceptable in a pre-COVID world and construction planners have learned from prior cycle excesses. ‘Beds and Sheds’ is a theme that over the last couple of years has benefited from supply-demand dynamics and an investor belief that strong rent growth and inexpensive debt capital would yield an opportunity for valuations to expand. And well, they were right! Beginning in 2020, annual rent growth in the apartments and industrial markets each hooked meaningfully higher, helping to expand valuations in a benign debt market.

Today’s market has a different backdrop. Rent growth in the ‘beds and sheds’ theme is still elevated and valuations e.g., cap-rates, essentially a property’s net operating income as a percentage of its market value, continue to be near unprecedented levels. But as we all know, inflation has become a mainstream topic and interest rates are no longer at rock bottom levels. Currently, the 10-year government bond sits around the 3% level, compared to less than 1% at the end of 2020. In turn, leveraged real estate buyers, those using debt to purchase a property, are seeing returns threatened as financing costs are rapidly approaching annual income. This nuance doesn’t necessarily spell doom for the real estate market, but it does give rise to an emerging theme, cash, or at least low leverage, wins.

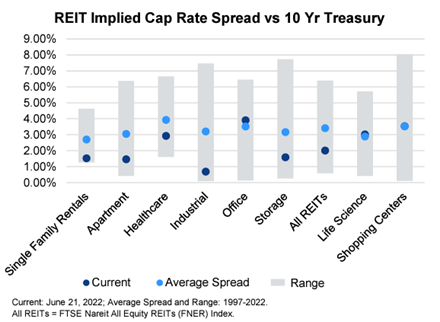

As we look toward the proverbial crystal ball, longer term we expect heightened supply in the ‘beds and sheds’ theme to stabilize rent growth and lead to a more rational valuation market. For example, over the past 25 years, the average spread between the valuation of the “beds” part of the theme and the U.S. 10-year government bond was roughly 3% - today, it’s closer to 1%. Same goes with the industrial market, historically the valuation spread has been close to 3%, but today, it is sub-1%.

In the near term, however, we believe structural dynamics in both markets remain attractive. For example, there is a fundamental shortage of four million housing units, according to Blackstone that has been “building” since the Great Financial Crisis. With respect to eCommerce and supply chains, each represent a structural growth story to the industrial market and like housing, the available supply doesn’t meet demand.

We continue to like the real estate market and subscribe to the belief that the near-term supply / demand dynamics within the ‘beds and sheds’ theme presents an attractive opportunity, but it’s important to be disciplined and alert with respect to future supply dynamics.

All opinions expressed in this article are for general informational purposes and constitute the judgment of the author(s) as of the date of the report. These opinions are subject to change without notice and are not intended to provide specific advice or recommendations for any individual or on any specific security. The material has been gathered from sources believed to be reliable, however Telemus Capital cannot guarantee the accuracy or completeness of such information, and certain information presented here may have been condensed or summarized from its original source. PAST PERFORMANCE IS NOT A GUARANTEE OF FUTURE RESULTS. Investment decisions should always be made based on the client's specific financial needs, goals and objectives, time horizon and risk tolerance. Current and future portfolio holdings are subject to risk. Risks may include interest-rate risk, market risk, inflation risk, deflation risk, currency risk, reinvestment risk, business risk, liquidity risk, financial risk, and cybersecurity risk. These risks are more fully described in Telemus Capital's Firm Brochure (Part 2A of Form ADV), which is available upon request. Telemus Capital does not guarantee the results of any investments. Investment, insurance and annuity products are not FDIC insured, are not bank guaranteed, and may lose value.

Advisory services are only offered to clients or prospective clients where Telemus and its representatives are properly licensed or exempt from licensure. No advice may be rendered by Telemus unless a client service agreement is in place. All composite data and corresponding calculations are available upon request.