Telemus Weekly Market Review September 4th - September 8th, 2023

The current contract between the United Auto Workers (UAW) union and the major auto companies is set to expire this coming Thursday. Thus far in 2023 there have already been meaningful labor agreements that have set a precent for where wage levels may be headed. The most notable labor agreements were with UPS drivers and American Airlines’ pilots, where both parties netted sizable salary adjustments. The combination of a shortage of workers alongside outsized inflation over the past two years has resulted in labor unions seeking more sizable wage and benefit adjustments.

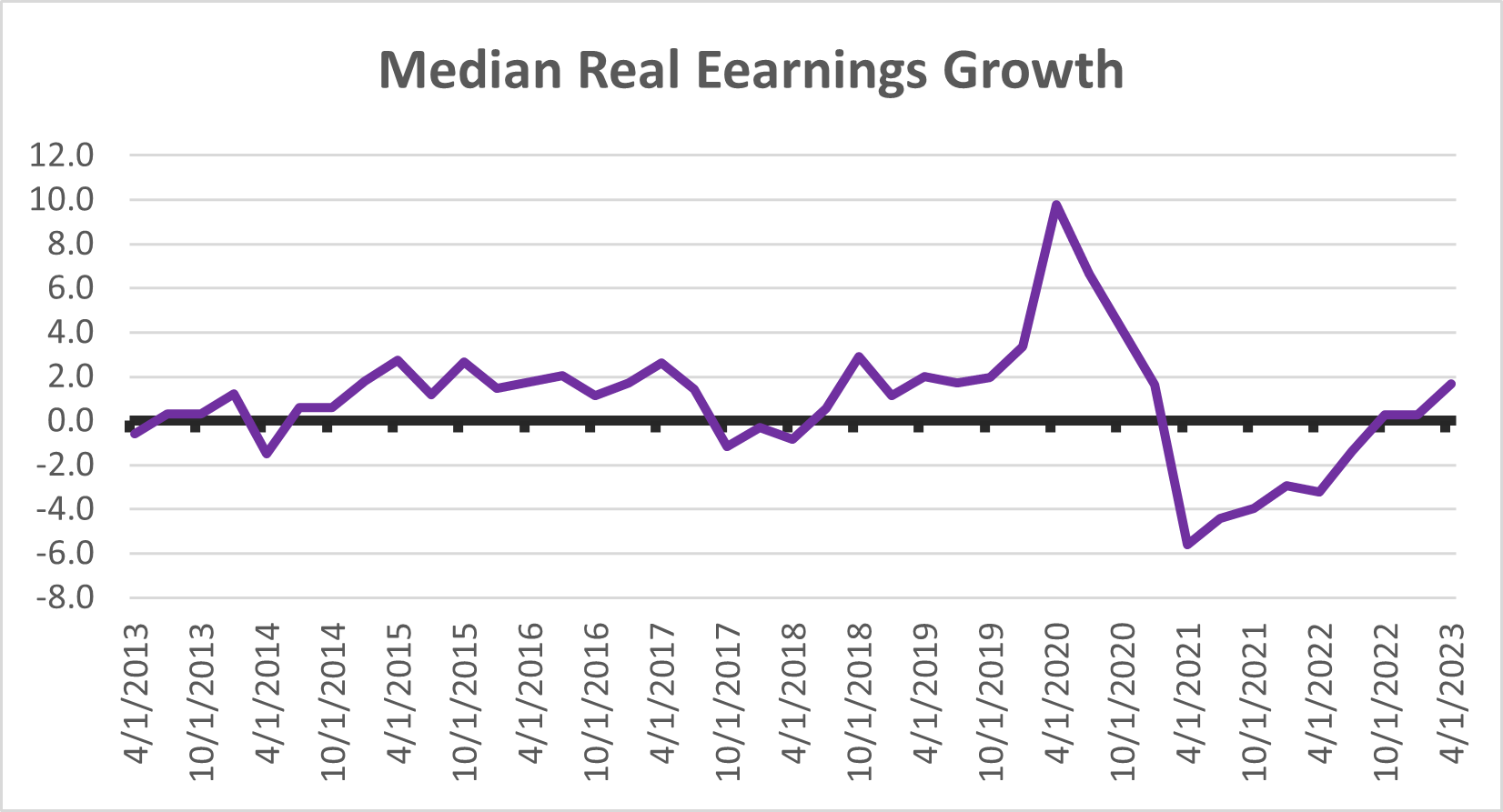

During 2022 the annualized rate of inflation spiked to just over 9%. For the average worker this calculated out to be a decline in their earnings power. For example, those that received a 5% raise were still 4% behind after accounting for the fact that goods and services cost 9% more. Only in the last quarter have real wages turned positive (see chart below) as a 4.3% increase in average hourly earnings over the past year is now higher than the 3.2% annualize rate of inflation. As labor contracts come up, not only are labor negotiations centered on catching up from lost purchasing power, but also putting in place annual wage increases that protect workers should inflation remain elevated.

Source: Bureau of Labor Statistics, St. Louis Federal Reserve

Recently negotiated labor contracts provide some perspective on precedents that may influence the UAW and automakers expectations as they negotiate terms. For example, the Teamsters union’s new agreement with UPS will result in the median salary for a driver reaching $49 an hour by the end of the contract. This compares to the current UAW contract where the highest wage tier is $32 an hour. While there will be dispersion in wages across companies and industries, terms set in recently negotiated contracts are likely to influence not only UAW negotiations but labor agreements in other industries as well.

Given the labor negotiations that have transpired to date, we expect there to be meaningful upward pressure on wage levels, which will have an influence on inflation. Moreover, longer-term negotiated annual raises that carry several years into the future are likely to serve as a more sustained and persistent inflationary influence. From the corporate standpoint, management teams will need to respond either through raising prices or sacrificing on profit margins. Price hikes are possible, and in the case of UPS they responded to the labor agreement by raising average prices by 6.9%. However, not all companies may be able to pass through the full impact of higher wages. Customers may not accept them, or companies may be unable to charge more especially if they face competitors with different labor dynamics. Moreover, as inflation has fallen over the past year, customers are going to be more reticent to accept price hikes without considering alternatives. Therefore, we expect rising labor costs to come at a detriment to corporate margins. Not all companies will face the same wage pressures and thus we could see margin fluctuations vary by company and industry.

In the case of the current UAW negation, concerns are rising that a strike may occur and have negative ramifications on the economy. What makes the current circumstance more significant is that the UAW’s contract expires with all three major auto manufacturers at the same time. Should a strike cause all three to halt production concurrently, this could ultimately create supply chain challenges as new car inventories decline. Used cars can step in as a substitute, although a surge in demand might lead to a significant acceleration in prices consistent with what was experienced coming out of the pandemic. An offsetting inflationary factor would be a drop in raw material demand. Hot-rolled steel, for example, would see a sizable decline in demand and would likely face price headwinds. During the strike at General Motors in 2019, the price of hot-rolled steel fell 17%i. Given the risk that all three automakers may face a strike at the same time, select commodities might face meaningful downside potential.

Individual labor negotiations tend not to have a widespread impact on the economy or markets in general. Given the significant wage hikes that came out of the UPS and American Airlines negotiations, along with the potential range of wage gains that may stem from the UAW negotiation, this time around there may be more significant long-term impacts on both inflation and corporate margins. We see this as a growing challenge for corporations and one of the reasons the Federal Reserve is reluctant to begin tapping the brakes on interest rates. Rising wage pressures appears likely to be a trend that will have some staying power in the months to come.

iSource: Bloomberg

All opinions expressed in this article are for general informational purposes and constitute the judgment of the author(s) as of the date of the report. These opinions are subject to change without notice and are not intended to provide specific advice or recommendations for any individual or on any specific security. The material has been gathered from sources believed to be reliable, however Telemus Capital cannot guarantee the accuracy or completeness of such information, and certain information presented here may have been condensed or summarized from its original source. PAST PERFORMANCE IS NOT A GUARANTEE OF FUTURE RESULTS. Investment decisions should always be made based on the client's specific financial needs, goals and objectives, time horizon and risk tolerance. Current and future portfolio holdings are subject to risk. Risks may include interest-rate risk, market risk, inflation risk, deflation risk, currency risk, reinvestment risk, business risk, liquidity risk, financial risk, and cybersecurity risk. These risks are more fully described in Telemus Capital's Firm Brochure (Part 2A of Form ADV), which is available upon request. Telemus Capital does not guarantee the results of any investments. Investment, insurance and annuity products are not FDIC insured, are not bank guaranteed, and may lose value. Any reference to an index is included for illustrative purposes only, as an index is not a security in which an investment can be made. Indices are unmanaged vehicles that serve as market indicators and do not account for the deduction of management fees and/or transaction costs generally associated with investable products. The S&P 500 index includes 500 leading companies in the US and is widely regarded as the best single gauge of large-cap US equities.

Advisory services are only offered to clients or prospective clients where Telemus and its representatives are properly licensed or exempt from licensure. No advice may be rendered by Telemus unless a client service agreement is in place.